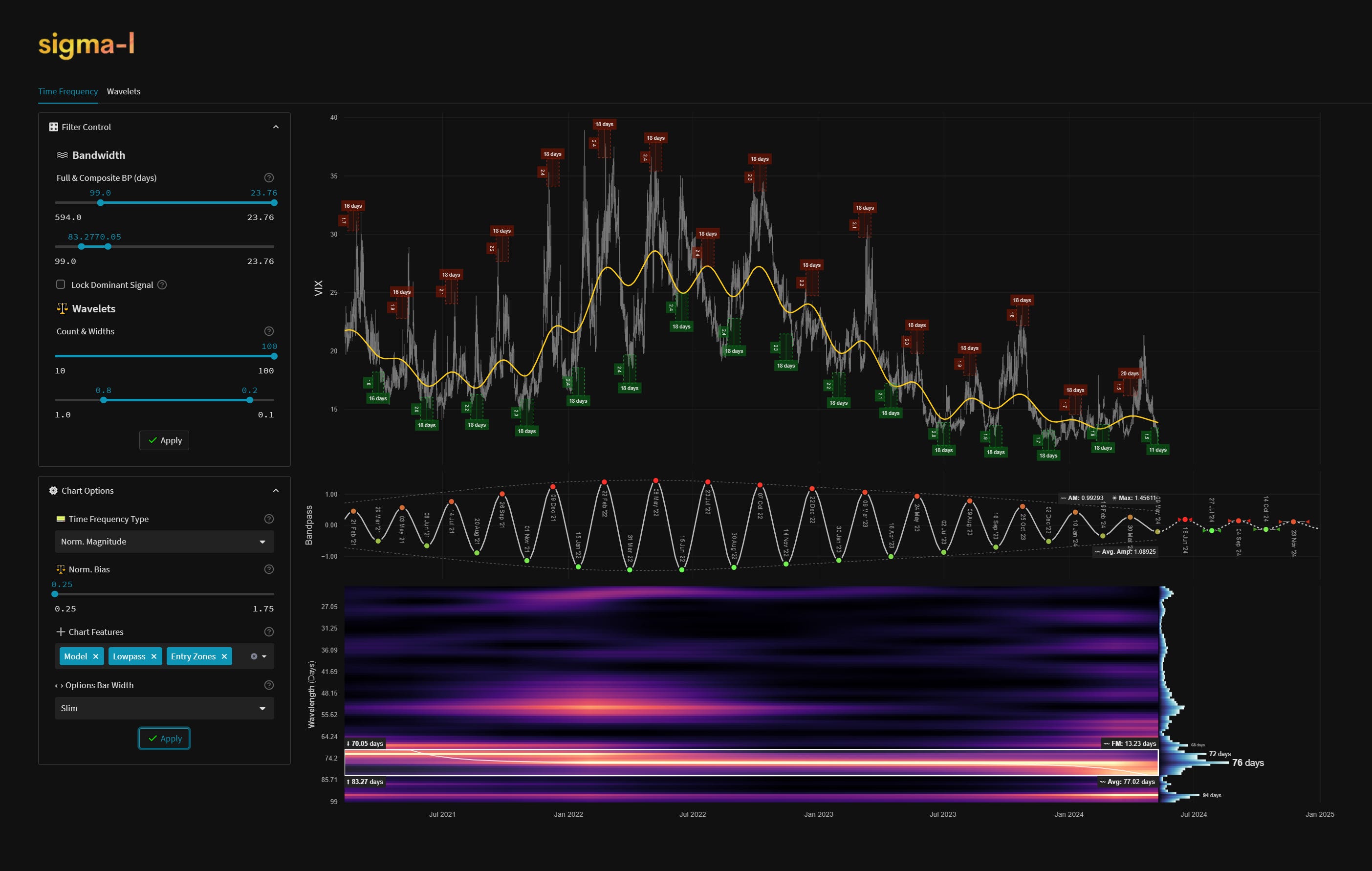

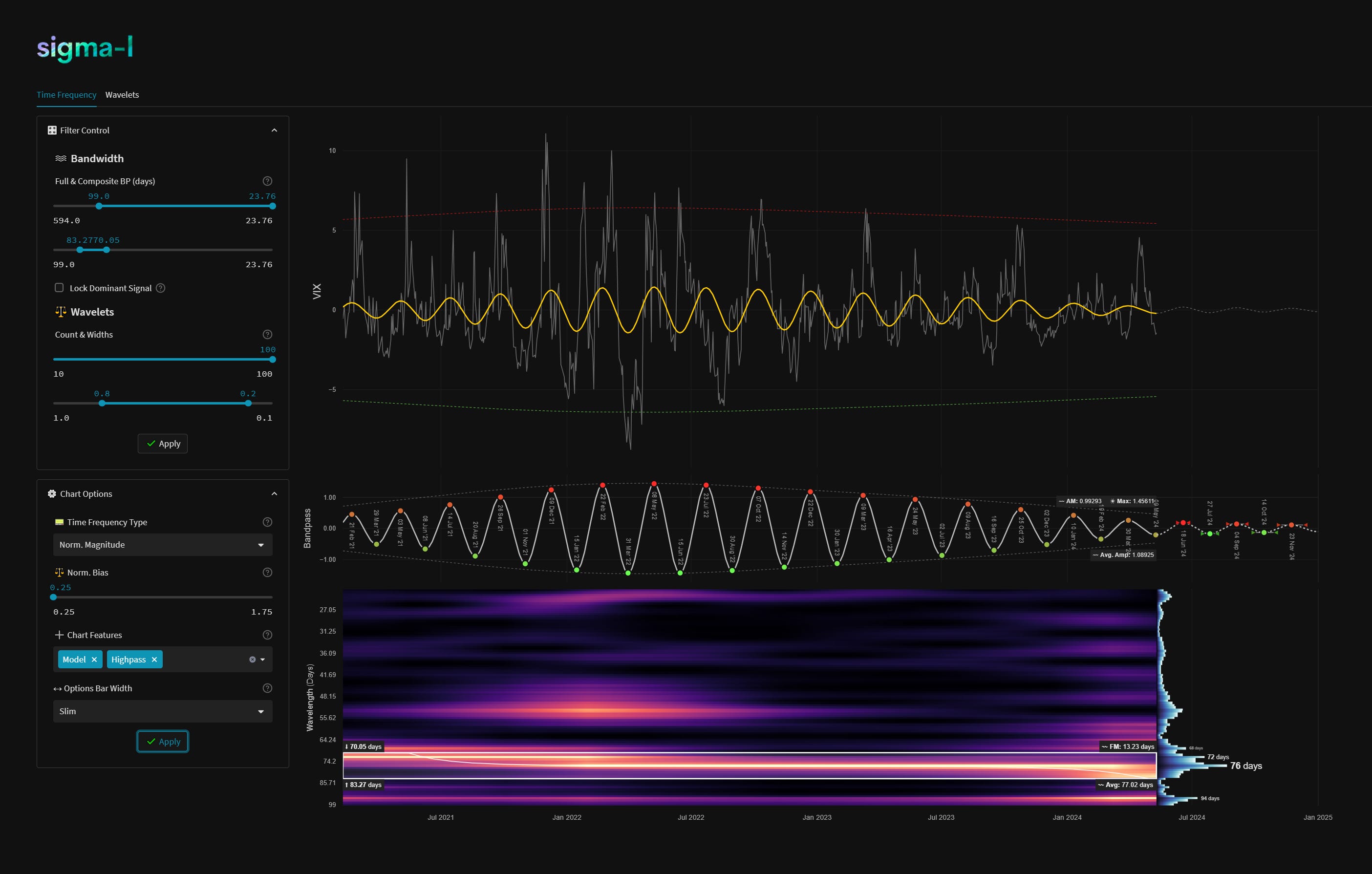

CBOE Volatility Index (VIX) - 10th May 2024 | @ 77 Days

'B' class signal detected in CBOE Volatility Index (VIX). Running at an average wavelength of 77 days over 15 iterations since February 2021. Currently troughing.

ΣL Cycle Summary

This excellent signal, amplitude modulated a touch recently by some higher frequency components, continues to beat well. Ostensibly an inverted representation of the Hurst 80 day nominal wave in stock markets, the undulations here are a good clue as to the direction of global equities and indeed the amplitude of any ensuing move. We saw in the last iteration of this wave a spike in power which caught many off guard, this is the nature of the VIX and it’s methodology, it can produce high yields quickly. The fact it also captures an inversion of the apparent periodicity in the S&P 500 (and therefore other global markets in general) is remarkable.

Time Frequency Analysis

Time frequency charts (learn more) below will typically show the cycle of interest against price, the bandpass output alone and the bandwidth of the component in the time frequency heatmap, framed in white. If a second chart is displayed it will usually show high-passed price with the extracted signal overlaid for visual clarity.

Current Signal Detail & Targets

Here we give more detail on the signal relative to speculative price, given the detected attributes of the component. In most cases the time target to hold a trade for is more important, given we focus on cycles in financial markets. Forthcoming trough and peak ranges are based upon the frequency modulation in the sample (learn more).